The Benefits of Financial Internal Controls in a Small Business

Cash is King/Queen in a small business. In an owner-managed business, working “on” the business vs. “in” the business is hard to do. You are so concerned with increasing revenues and keeping costs at a manageable level, that sometimes other operational areas are put on the “to do” list for a later day. However, having some financial controls in place is a good idea. The main purpose of these controls or procedures is to ensure that the cash earned in the business is protected. It also ensures accuracy in financial reporting and minimizes the risk of fraud or error. For small businesses, where resources are often tight, effective internal controls can mean the difference between survival and failure.

Here are some benefits of implementing financial internal controls in a small business:

Protection Against Fraud

One of the primary purposes of internal controls is to reduce the risk of fraud. Fraud can take many forms, from employees misappropriating funds to unauthorized purchases made on company credit cards. Small businesses, especially those with fewer employees, are often more vulnerable to fraudulent activities because a single person may have too much access over critical functions, like bookkeeping and financial reporting.

By implementing separation of duties—one of the cornerstones of internal controls—a business ensures that no single employee has complete control over any financial process. For instance, the employee who receives cash at the cash register during the day should not be the same person that reconciles the daily cash to sales at the end of the day.

Improved Accuracy in Financial Reporting

Accurate financial reporting is essential for informed decision-making. Internal controls such as regular account reconciliations, proper documentation of expenses, and reviews of financial statements ensure that the information on which you base your business decisions is reliable.

Having accurate records not only helps you understand your cash flow and profitability but also provides you with credible data when seeking loans or investors. Financial accuracy also ensures compliance with tax laws, reducing the risk of costly penalties and audits. An example of a control, would be to perform monthly bank reconciliations on all bank and credit card accounts. This ensures that transactions are recorded accurately and completely in your books and records. This exercise would also allow the person reconciling the account to identify any significant or unusual transactions that do not look appropriate.

Operational Efficiency

Effective internal controls contribute to operational efficiency by streamlining financial processes. When procedures are clearly defined and automated where possible, employees can perform their tasks more quickly and accurately. For example, having a well-documented purchase approval process can reduce delays in procuring materials or services, keeping projects on track. In a small business, this could be that the person who is placing the order needs to have approval from the business owner before finalizing the order. This approval could be done with an e-signature, or even an email. Approval by text is not as effective since it’s hard to refer back to it if there is a question as to whether or not approval has been given.

Additionally, automation tools like accounting software can enforce internal controls by requiring certain steps to be completed before moving forward, ensuring compliance and reducing human error.

Enhanced Accountability

Internal controls promote accountability among employees. When everyone in the organization understands the procedures and is held to a high standard, there is less room for mistakes, negligence, or misconduct. Clear, documented processes make it easy to track who is responsible for each financial transaction, reducing the likelihood of disputes and finger-pointing when things go wrong.

In small businesses, this is particularly important because owners often have a close working relationship with their staff. Transparent accountability helps maintain trust and ensures that any financial discrepancies are identified and addressed promptly. An example of this would be to have the internal controls documented in an employee handbook or a procedure manual that all employees have read.

Other reasons to have internal controls

Lenders and external investors: If they understand that your business already implements financial internal controls, they will have more confidence in you as a business owner. They understand that you understand the importance of safeguarding your company’s funds.

Tax Audits: Overall, tax auditors don’t care whether or not your business has any financial controls in place. However, when there is a request for information from a tax auditor, having financial controls in place will help you find the information you are looking for in a more efficient manner. And as a result, will allow you to have the tax auditor finish their work more quickly. It also gives them confidence that you are a fiscally responsible business owner.

Conclusion

In the fast-paced world of small business, it’s easy to prioritize growth and customer acquisition over back-end processes like financial controls. However, without effective internal controls, your business is vulnerable to fraud, errors, and inefficiencies that could derail your success. By investing in financial internal controls early, you protect your assets, ensure accurate reporting, and set your business up for sustainable growth.

Internal controls are not just for big corporations; they are a vital tool for small businesses to maintain financial health and thrive in a competitive market.

Please reach out to us at [email protected] if you would like us to talk to you about your company’s internal controls.

The Benefits of Financial Internal Controls in a Small Business Read More »

Things to Consider When Picking a Corporate Tax Year-end

When you create a company, you have the opportunity to determine when you would like the fiscal period to end. The general default for a person is to select December 31st as the year-end.

However, there are some other factors that you should consider when selecting a year-end date.

You have 365 days from the date of incorporation to select your year-end. And it is set once you file your first corporate tax return. But you can pick any day within that 365 day period to be your year-end.

One factor may be based on how your revenues are earned during a year. Ideally, you should be targeting your year-end to coincide with the end of a busy period where there is a bit of “calm”. This will allow you to gather up all of the paperwork for the year and to have the time to reflect on the activities in the year to make sure that everything has been captured.

You don’t want to have a drawn out year-end close process. Our memories can sometimes deceive us and the longer period of time between when you close a fiscal year for your company and when the actual fiscal year-end occurs, facts can be forgotten. Therefore, it is important to close off the books and records as soon as possible. This will also help you plan better for the upcoming year.

Some questions for you to consider:

- Is your business seasonal?

- For example: Is you business busiest during a school year? (September – June)

- Are the defined cycles to your business?

- Busy Spring & Summer, but slow Fall & Winter?

- Is your business tied to a government payment schedule or a government grant where you need to provide reporting to them based on their fiscal year-end?

- Most governments have a March year-end

- Is your busiest time of business in December?

If you are a retail based business or a restaurant, the industry standard is to have a January or February year-end. This allows your business to have the time to incorporate your most profitable periods into your business.

If your business earns most of its revenue supporting school-aged children during the in-session periods, then maybe a June/July year-end is best for you.

But what is a good year-end if your business is fairly consistent month over month, or there isn’t any consistency to revenues? Then you may opt for a month that suits your lifestyle. If you like to go away in January, maybe select a year-end that isn’t December or January. If you like to have your summers off, my suggestion would be to avoid the months from May – July as your fiscal year-end.

An additional point to consider when picking a fiscal year-end is a potential tax planning opportunity. If your business has an unusual year where there is higher than normal revenues, you have the opportunity to spread out how to withdraw that money for your personal purposes over more than one year.

So before you pick December 31st as your fiscal year-end, make sure you take the time to look at your business plan to see if there is another month that would be preferable. Taxes and accounting are hard enough to keep on top of when you are running your own business. So be kind to yourself and make sure that you are selecting the year-end that works best for you.

If you’d like to brainstorm this with someone, please feel free to reach out to us at [email protected].

Things to Consider When Picking a Corporate Tax Year-end Read More »

Tax Benefits of Purchasing Life Insurance through your Corporation

Life Insurance is a great thing to have. Especially from a tax perspective. When you personally purchase a life insurance policy, and you die, your beneficiaries receive the amount of the policy and it is a tax-free receipt of cash to them.

Certain policies purchased provide beneficiaries with sufficient cash to fund tax liabilities that you may leave behind in your estate (if your estate doesn’t have enough liquid cash to pay for the tax). This way, the family home doesn’t have to be sold just because you’ve passed away.

Life insurance can also be purchased by a company. If you own your own business, having your company purchase life insurance may be an advantageous tax planning strategy. The benefits of the company purchasing the life insurance on your behalf is that the premiums are paid with the company’s money and not your personal money, which makes it less expensive for you since it is being paid with pre-tax dollars, although an add back for the premiums is typically required when calculating taxable income. The proceeds of the life insurance could be received by the company on a tax-free basis and may be distributed to your beneficiaries on a tax-free basis through the corporation’s Capital Dividend Account. The proceeds may also be used to pay for any existing liabilities in the company that need to be settled subsequent to death.

There may be some other benefits as well, depending on the type of life insurance policy as this is a discussion that would be best to have with an Insurance Specialist.

If you have any questions, please reach out to us at [email protected].

Tax Benefits of Purchasing Life Insurance through your Corporation Read More »

Changes to how Rental Properties will be Taxed

In the Fall Economic Update statement (November 2023), it was stated that certain deductions were no longer going to be allowed after January 1, 2024. These rules became law on June 20, 2024 under Bill C-59. The legislation denies many expenses if you are not following the rules…

For the purposes of the Income Tax Act, rental properties located in an area where short-term rentals are not allowed are defined as “non-compliant short-term rental” properties. The definition of a short-term rental is for a property to be rented for a period of less than 90 consecutive days.

The portion of the expense that will not be deductible, is based on a formula.

Total of ALL EXPENSES incurred x # of days in the taxation year that the property was a non-compliant property / the number of days in the taxation year that the property was a short-term rental.

Generally, the following expenses would be allowed:

- Advertising expenses

- Insurance premiums

- Office expenses

- This would include pens, paper and other stationery types of items

- Legal expenses

- Legal services used to collect outstanding rent payments

- Fees to purchase a property are NOT an allowed deduction

- Accounting fees

- Bookkeeping services

- Preparation of the rental statement for your tax return

- Property management fees paid to an external party

- This includes strata fees

- Repairs and maintenance

- Your own labour costs are NOT an allowed deduction

- Wages of the person you pay to maintain your own property

- Don’t forget that you should be making withholding tax payments and submitting a T4Summary for these wages.

- Property taxes

- Travel expenses to get to your property

- Not meals and accommodation

- Utilities

- Bank charges

- To maintain the bank account used for rental income and expenses

- Interest expense to finance the property

If you operate a short-term rental property that exists in an area where short-term rentals are not allowed, the expenses incurred will not be allowed to reduce your rental income. You would be considered to have a non-compliant short-term rental property. If the local government where you own your property allows for short-term rentals if you meet certain conditions (i.e. business license), then your property will become a compliant short-term rental. Once it is a compliant short-term rental, you will be able to claim the above expenses as a deduction from your rental income.

Example:

| Old Rules | New Rules – Compliant Short-term Rental | New Rules – Non-Compliant Short-term Rental | |

| Rental income | 20,000 | 20,000 | 20,000 |

| Mortgage interest | (4,000) | NIL | (4,000) |

| Property taxes | (2,000) | NIL | (2,000) |

| Utilities | (1,500) | NIL | (1,500) |

| Net Rental income for Tax Purposes | 12,500 | 20,000 | 12,500 |

So you will pay tax on $20,000 of net rental income if you are non-compliant, compared to only paying tax on $12,500 of net rental income if you are compliant.

Changes to how Rental Properties will be Taxed Read More »

2024 Federal Budget: Changes to how Capital Gains are taxed in Canada

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your tax advisor to discuss specifics to your situation and for fact appropriate advice.

NOTE: This post assumes that the Tax Measures announced in the April 2024 budget will be passed as presented. If any changes occur, we will update this article.

The 2024 Federal Budget was announced in April, which is already a busy time for accountants, so you can imagine how pleased the tax community was to find out that this particular Budget was going to make some major changes to how Capital Gains are being taxed in Canada.

In summary, as of June 25, 2024, if you are a corporation, 66.67% of a Capital Gain will be taxed in Canada. If you are an individual, you get a bit of a reprieve. The first $250,000 of capital gains, will have an income inclusion of the historical 50% rate, but any capital gains above this $250,000 amount will be included in income at 66.67%.

If you have a holding corporation that has a larger portfolio of investments, it is a good idea to meet with your financial advisor and accountant to discuss how to manage your company’s tax liability for 2024. It may be a good idea to trigger losses. But just make sure you don’t inadvertently create superficial losses that can’t be used in the current year.

For individuals, and the average Canadian, the likelihood of earning more than $250,000 in Capital Gains in a single year is on the lower end. However, if you have a rental property that you are selling or potentially, an investment in a private company was sold, you should be aware of these rules and you should reach out to your accountant for support on what this means.

If you have capital losses that were realized before June 25, 2024, those losses will still be available to offset capital gains realized at the 66.67% inclusion rate.

Example: Sara owns a rental property in Kelowna, BC and is a resident of BC. Due to the Federal Underused Housing Tax, and the BC Speculation and Vacancy Tax filing requirements, she’s decided that she no longer wants to own this property. She lists the property in April 2024. If she is able to sell and close on the sale before June 25, 2024, her taxes will be significantly different compared to if she sold their rental property after June 25, 2024.

She purchased the property in March 2021 for $400,000 and the current market value of the property is $1,000,000. We’ll perform our analysis as if she sold the property at its current market value.

You’ll see that Sara’s tax liability would have increased by 22% had she waited to dispose of the property until after June 25, 2024.

Affirm LLP and Affirm Wealth Ltd. are now proud and independent members of the Integrated Advisory Network and would happily meet with you if you would discuss your current situation and how to minimize the tax impact this year.

2024 Federal Budget: Changes to how Capital Gains are taxed in Canada Read More »

Short-term to Long-term Residential Rental Accommodations – GST/HST Implications

When the Federal government delivered their 2023 Fall Economic statement, they proposal that certain deductions on short-term residential rentals would no longer be allowed. This is one way that the Federal Government is trying to create more housing for people living in Canada. The belief is that the short-term rental market is impacting the number of longer term rental units that are available and affordable for people living and working in Canada. In addition, we are seeing provincial and municipal proposals to levy hefty fines to try to encourage the conversion from short term rentals to long term rentals. As a result, we’ve noted that some of our clients are wanting to switch from short-term rentals to long-term rentals.

However, there are some significant implications from a GST/HST perspective. Unfortunately, GST/HST does get overlooked, since it isn’t an area of taxation that many of us deal with on a day to day basis. This is where it pays to be curious about potential consequences.

For short-term rentals, any income earned on short-term rentals are subject to GST/HST as it’s considered a commercial activity. This means that when you rent your property on a short-term basis, you are required to collect GST/HST on these stays. Those individuals that are utilizing platforms like Airbnb and VRBO to manage their rental properties, the GST/HST is usuallybeing collected and remitted on behalf of the property owners. (This assumes that the Taxpayer has exceeded the $30,000 small supplier threshold or has registered for GST voluntarily)

When you have a long-term residential rental unit, the income earned is exempt from GST/HST. “Long-term” is anything where the stay is more than 60 continuous days. You would think that this is a positive change. One less tax filing that you will have to do in the future. However, in switching from a short-term rental to a long-term rental arrangement, or any change in use greater than 10%, you have changed the nature of the property. Since you are no longer collecting GST/HST, due to the change in the type of income you are earning, you have changed the use of the property. And as a result, you have to “dispose” of the short-term rental property and then “acquire” the long-term rental property. At the time of the change in use, you are required to pay GST/HST on the Basic Tax Content of the property to the CRA. This also applies to long-term rental properties that become short-term rental properties. At the point in time that it is no longer a long-term rental property, GST/HST on the Basic Tax Content of the property needs to be remitted to the CRA.

There was a recent court case that confirmed the application of assessing 5% GST on the property when it changes use from a short-term residential property to a long-term residential property (1351231 Ontario Inc. and His Majesty the King, 2020-2180(GST)G). In this case, the taxpayer had a condo unit that was a long-term rental and then became a short-term rental and the taxpayer did not remit the GST/HST at the time of the change in use. The court ruled in favour of the Government and therefore, the taxpayer needed to pay the GST/HST plus interest and penalties.

NOTE: This is applicable to Residential Rental units. Commercial Rental Units have a different treatment for GST/HST.

Short-term to Long-term Residential Rental Accommodations – GST/HST Implications Read More »

What to expect during a CRA Tax Audit

The dreaded Canada Revenue Agency audit. Everyone, including us, get a bit anxious when we receive a letter from the CRA informing us that a client of ours is going to be visited by their staff to perform an audit of their financial records. But realistically, there shouldn’t be too much for us to worry about since we’ve all been through the process a number of times before.

What we’d like to be able to do in this blog post is to give you a bit guidance as to what you can expect and how the process works.

Desk Audits vs Full Audits

Generally speaking, a desk audit will look at a specific period of time and a specific issue. A common desk audit would be a payroll audit or a GST audit. The most common GST desk audit is when you file your first GST return and it’s in a refund position. The CRA will generally request for a description of your revenues and as well as the 10 largest invoices as well as the 10 largest supplier invoices that they can review to ensure that you’re calculating and remitting the GST appropriately.

A Full Audit will generally be for an entire fiscal year and can expand to include a Payroll and GST audit depending on what the income tax auditor discovers. A Full audit may involve having an Income Tax Auditor spend time in your offices. It should be noted that since the COVID-19 pandemic, there are been fewer in-person audits from the CRA.

How it starts:

You will receive a letter from the Canada Revenue Agency to let you know that you or your company has been selected to have an audit performed. Check the date of the letter. You generally are given 30 days to pull together the initial information that the auditor will require. Make sure that you notify your external accountant as soon as possible so that they can help you through this process.

The initial request will be to provide information for a particular period of time. There will be a request for tax returns as filed, the trial balance, general ledger. The time period requested, will generally be for one of the previous 4 years. The CRA has a mandate that they will not audit a period older than 4 years from the last year-end unless they discover something blatantly erroneous. Then they will look at older years.

Timing:

Any time an audit occurs, it generally isn’t a great time of year. And working with the auditor will take time away from you operating your business. However, there are times that are better than others. If it’s an exceptionally busy time for you and your business, you can request an extension of time to respond to the information request. Most auditors will appreciate that their timing may not work for you.

Tips in Working with the Auditors:

- Have the auditor explain things to you. Make sure you understand why they are asking for items and also use this time to help educate them on your business. In many instances, the auditors can help you with improving your accounting systems.

- When an auditor requests for information, make sure that they make the requests in writing. Verbal requests are common, but sometimes the auditor will request for information that they may or may not actually need for their auditing procedures. You should also respond to all requests in writing. You can respond verbally, but this should also be followed up in writing. If in the future, you need to rely or challenge something from this audit, you will need to have written support to support you claims.

- While the auditors are looking for errors, they can be useful to you and your business. If there is something that you may not have deducted from your income because you weren’t sure if it was an allowed deduction, ask them. If it is a deductible expense, they will help you adjust your return so that it reflects the additional expense.

- Don’t drag your heels when responding to their questions. If you know that it will take time to produce the information that they are looking for (i.e. need to request the information from storage; or if you are working on a larger project at work), let them know that it will take some time to get back to them.

- Just remember, that the longer that it takes to get back to them, there could be more areas that they will look at as they are waiting on your information.

Wrapping up the Audit:

Once an audit is completed, you’ll receive a letter from the auditor. It will summarize their findings and what the next steps would be. This will generally mean that the audit is finished.

If there were a number of errors found, you can expect that another CRA audit will likely happen in the near future. If the number of errors found were minimal, you shouldn’t expect to hear from the CRA for a number of years.

If a number of errors were found in your income tax audit, you can also expect to be contacted by the Payroll Auditors and the Excise Tax Auditors (GST/HST).

What to expect during a CRA Tax Audit Read More »

Benefits and Disadvantages of a Joint Spousal and Alter Ego Trust

Note: This blog post is information that is directed towards those individuals who have assets in BC and Ontario, but may be of interest to others as well.

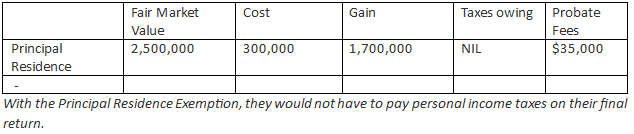

If you are over 65 years of age, an Alter Ego Trust or a Joint Spousal Trust can be used to assist with your Estate Tax Plans and to help minimize the taxes due on your death as well as assisting in avoiding Probate Fees. Probate fees in BC are 1.4% of the Fair Market Value of the assets in a person’s estate. But like anything, there are advantages and disadvantages of creating one of these trusts.

Advantages:

These trusts can save your estate money when you die.

Asset Held Personally

Assets held in a Trust

Total cash savings when assets are in the trust is $35,000.

Ideally, we feel that this is a good option if your principal residence is worth more than $2.5 Million dollars. The savings on probate fees will outweigh the administration costs of maintaining the trust year to year.

There are other assets that could also be put into these trusts, but we would need to review this on an asset by asset basis.

These trusts will also allow you to live as you normally would. You can stay in your home and you still receive income from the assets that are placed in these trusts.

Some additional non-financial reasons why you might consider using a joint spousal trust or an alter ego trust in your estate planning is for privacy or in the instances of blended families. Assets in these trusts are not subject to public probate records nor can they be contested by beneficiaries. These trusts are also useful where there are adult children and the parent remarries and wants to ensure the new spouse can enjoy use of the family home and other assets until the spouse’s passing, after the spouses’ passing the assets can be distributed to children.

Disadvantages:

The biggest disadvantage of creating these trusts are the tax rates that these trusts pay on the undistributed income earned during a tax year. Trust income is taxed at the highest marginal tax rate for individuals, based on where the trust is located. In Alberta the top marginal tax rate is 48.%; in BC, it is 53.50%; and in Ontario, it is 53.53%.

The trusts can usually avoid paying tax at these rates by distributing their income out to the beneficiaries of the trust during the year.

An additional disadvantage is the cost to maintain the trust every year, by filing additional tax returns and paying any trustee or other administration fees. The trust is effectively a separate legal entity that must be maintained separate from your personal affairs.

The last disadvantage that we wanted to mention in this blog, is the differences that occurs when you die and your assets have been held personally, compared to when you die and your assets are held in a Trust.

When you die with a regular will, there is a deemed disposition of all your financial assets at their fair market values on that date. The gains and losses on these assets are realized on your final personal tax return and are automatically acquired by your Estate at those fair market values. The Estate is then administered by your executor/executrix as outlined in your will. From a tax perspective, your Estate is eligible to be treated as a Graduated Rate Estate and is taxed as an individual would be however, without the benefit of any personal tax credits. This means that the estate would be taxed on the same graduated tax rate schedule as an individual. This only lasts for 3 years and after the first 36 months, the tax rate defaults to the highest marginal rates.

Conversely, if you die and your assets are in a Joint Spousal Trust or an Alter Ego Trust, the assets in these Trusts are not eligible for these same graduated rates. Upon death, the assets in the Joint Spousal Trust or Alter Ego Trust will be taxed at the highest marginal tax rate; the assets will then be distributed from this Trust in accordance with the instructions in the trust indenture. The Joint Spousal Trust and Alter Ego Trust assets are held separate from the estate so the Trust assets will bypass any application of the last will and testament of these assets. It is therefore very important that the Trust Indenture and the Last Will and Testament be updated at the same time to ensure there is no conflict between these two very important legal documents.

This is a very simplified summary of some of the advantages and disadvantages that a Trust can provide to taxpayers and our belief is that, while there are some disadvantages to having a Joint Spousal Trust or an Alter Ego Trust, the cash tax savings should not be ignored. And many of the potential disadvantages just need to be analyzed to ensure that the cash tax savings still exists. If this is something that is of interest to you, please feel free to reach out to us to discuss further.

Benefits and Disadvantages of a Joint Spousal and Alter Ego Trust Read More »

Ch-Ch-Ch-Changes: Short Term Rentals, Bare Trusts and the Underused Housing Tax

Well, we’ve just received the Fall Economic Statement from our Government. In there, were a bunch of tidbits. And one change that was found on the CRA website that could be helpful to some taxpayers.

Short-Term Rentals

There is one in particular that I think was highly unfortunate to see. Mortgage interest is no longer an eligible expense if you use your home for short-term rentals.

Part of the 2023 Fall Economic Statement addressed the housing crisis that many Canadians are seeing with a lack of affordable housing. To combat this, the government is cracking down on short term rentals. Where short term rentals are prohibited, or where licensing/permits/registration requirements are required but where the taxpayer has not obtained appropriate licensing, the federal government intends to deny tax deductions incurred to earn short term rental income. This change is proposed for periods from Jan 1, 2024 onwards. As an example, if you own a short term rental and previously collected $100,000 of rental income, and had mortgage interest of $80,000, only $20,000 may be taxable. In 2024, if the short term rental falls subject to these rules, the entire $100,000 collected would be taxable. This could result in significant tax liability for the taxpayer.

Bare Trusts

I know that we discussed this in a previous blog post (see “You May now have a Trust Reporting Requirement Under the New Trust Reporting Rules”), but this is one of the areas that is causing a lot of concern for us at Affirm LLP.

A Bare Trusts is an entity or individual that holds title to something for the beneficial use of someone else. They are not considered to be “regular” trusts and do not have to have a formalized trust agreement. Nor have they had to file a Trust Return. However, as a part of the Budget and then formalized in Bill C-32, there are new trust reporting requirements that make it a requirement for these types of arrangements to file a tax return.

As of this month (December 2023), the CRA has created a new FAQ type of page to help all of us work through what needs to be reported and how to report it. (https://www.canada.ca/en/revenue-agency/services/tax/trust-administrators/t3-return/new-trust-reporting-requirements-t3-filed-tax-years-ending-december-2023.html) According to the preamble on this page, it will be updated periodically, so it is expected that this is just the beginning of the information that they are going to provide to us. This is similar to how they managed the new Underused Housing Tax reporting requirements.

We can’t reiterate enough that if you do feel that you are in a Bare Trust arrangement, please reach out to your tax advisor and they can help you figure out what needs to be done to keep you compliant with the CRA.

Ch-Ch-Ch-Changes: Short Term Rentals, Bare Trusts and the Underused Housing Tax Read More »

You May Now Have a Trust Reporting Requirement Under the New Trust Reporting Rules

As of December 30, 2023, there are new Trust reporting rules that come into effect. In our opinion, the impact on those that are already filing a Trust Return will not be as great as those that are going to be filing a Trust Return for the first time.

Those that already are filing Trust Returns are affected, but they are already used to the process that goes into preparing a Trust Return. They will have an additional schedule to file with their 2023 Trust Return (Schedule 15) where they will have to disclose all of the parties that are involved in the trust. There will be some additional information gathering to ensure that we have all of the relevant information for each of the trusts that we’re filing on behalf of our clients, but overall, that isn’t what is causing all of the angst.

The stress within the tax community is on those people, corporations, and partnerships, that haven’t had to file a trust return in the past but will now have to do so. Trying to determine if a trust relationship exists, with minimal guidance from the Canada Revenue Agency (as of November 6, 2023), has been frustrating. Starting this year, Trust Returns will be required for those individuals or corporations that hold onto an asset for the beneficial use of another entity (individual, corporation or partnership). These types of relationships are generally referred to as Bare Trusts. Many people are finding out for the first time that they have a trust relationship.

Here are some examples of what a Bare Trust is:

- You have a corporation that holds title to a piece of land, but another corporation is using, enjoying and/or benefiting from the land.

- You have opened up a bank account for your grandchildren who are under the age of 18.

- You have added your adult child onto your investment accounts or bank accounts for probate purposes.

- You and your spouse made an investment with money you earned. Both of you are on title, but you are the only one that claims the income earned since it was your earnings that made the investment.

- This is correct for the purposes of the tax attribution rules. All of the income would be attributed back to you. But now you will have a trust filing because your spouse is on title.

- Your son or daughter has purchased a home and you are on title to that home as well in order to guarantee a mortgage for them. But you don’t live in that home or have any other rights to that home.

In these situations, you will need to file a Trust Return for 2023. The only one where you may not have to is if the bank account or publicly traded portfolio investment account have a balance that is under $50,000 at all times during the year. In many instances you will not need to file a Trust Return. However, even in this situation, you may find that you have to file a Trust Return, since certain investments qualify for the exemption, and others do not.

The good news is that in most Bare Trust relationships, there will be no tax due. It will be an exercise in disclosure. The bad news is that if you choose not to file the return, the penalties are severe. The penalties are $25 per day with a minimum penalty of $100 and a maximum of $2,500 per return. And since you chose not to file the return, there is an additional penalty of the greater of $2,500 or 5% of the maximum value of the property held during the year.

And just in case you were thinking that perhaps these rules will be deferred for a period of time? We aren’t that hopeful, especially since these rules have been hovering over us for the past few years, and finally got passed in Parliament at the end of last year.

If any of these situations apply to you, please reach out to us as soon as possible so that we can start applying for a Trust Account Number and ensure that you have all of the documentation that will be required to disclose on the Trust Return. Trust Returns with a December 31st year end are due March 30, 2024.

You May Now Have a Trust Reporting Requirement Under the New Trust Reporting Rules Read More »

Interpreting your Financial Statements – Statement of Cash Flows

Running a small business in Canada is no easy feat. It requires dedication, strategic planning and a keen eye for financial management. We’ve discussed the purpose and benefits of having and analyzing a Balance Sheet and Income Statement, but there is one statement that isn’t as common, but is just as important, the Cash Flow Statement, or the Statement of Cash Flow. This financial statement is one of the most all encompassing statements that a business can use to assess where their company has been earning and spending their money.

The Statement of Cash Flow is a financial report that provides a detailed breakdown of the cash inflows and outflows of your business during a specific period. It is typically categorized into three main sections:

- Operating Activities: This section focuses on the cash generated or used in day-to-day operations, such as sales, purchases and expenses.

- Investing Activities: This is where you will see if you made purchases or sold equipment, property or other investments.

- Financing Activities: This section deals with the cash flow from borrowing or repaying loans, issuing or buying back shares of your company or other financing-related activities.

The key benefits of maintaining and creating a cash flow statement for your business:

- The Statement can give you a really good summary of whether your business brought in more cash than it spent in during a fiscal period.

- Is your cash balance higher or lower at the end of the fiscal period?

- It will also breakdown for you as to how your business is generating its cash.

- Is it all from operations? Or was it supported from that additional line of credit or loan that your business took out during the year?

- Are your operations generating sufficient cash to satisfy its debt obligations?

- Is there positive cash being generated from your operations?

- If it’s negative,

- Is it because you have not collected on all of your outstanding Accounts Receivable?

- Or have you had to increase your marketing expenses?

- If it’s negative,

- It can also be used as a planning tool for the upcoming budget for future years.

- If you have minimal purchases of capital equipment this year, will you need to purchase additional/newer equipment in future years?

- If your cash from operations is negative or minimal,

- Do you need to increase your budget on advertising?

- Do you need to layoff staff?

- Or do you need to concentrate on collecting on your outstanding receivables?

- Do the terms of your financing change in the coming years?

- Will you need to seek out additional funds for your business?

- If so, can your business support the additional cash repayment terms that would be required of the company?

- Will you need to seek out additional funds for your business?

Overall, the Statement of Cash Flow is a very valuable tool that can empower you to manage your finances more effectively, make informed decisions, secure financing and pave the way for sustainable growth.

Interpreting your Financial Statements – Statement of Cash Flows Read More »

Interpreting your Financial Statements – The Income Statement

The next financial statement that we’ll tackle is the Income Statement. The Income Statement can go by many names, “Income Statement,” “Profit & Loss Statement” or the “Statement of Income and Retained Earnings” are the most common ones. Our firm calls it the Statement of Income (or Loss) and Retained Earnings.

What is the Income Statement?

The Income Statement provides an overview on the operations or activities of a business for a specific period of time. Each year a company will need to provide an annual income statement to report to the Canada Revenue Agency with their tax return and will end up paying income taxes based on the net taxable income that has been earned by that company. Publicly traded companies will report their Income Statements on a quarterly basis to their shareholders. Many companies, both private and public, will have their financials prepared on a monthly or quarterly basis to analyze how the business is performing and to assess if any trends can be seen in sales or costs.

Things to think about when preparing your Income Statement

Since the purpose of the income statement is to tell the story of how your business did during a particular period of time, it’s important to ensure that the amounts on the income statement properly reflect what happened during that time. Some key areas to consider are revenues, cost of sales or cost of service expenses, gross profit (profit margin), and overhead expenses (often fixed costs to run your business).

Revenues

On a high-level basis, if you’ve sold something, you should be recording it as revenue. However, there are some nuances that need to be considered that may change how much revenue is recognized. Here is an example. You are successful in signing a contract valued at $30,000 to deliver your services over a 6 month period, but your client pays you 50% up front and then 50% at the completion of the contract. How do you recognize the revenue? Do you recognize the $30,000 immediately? Or do you recognize the revenue on a monthly basis?

If the services provided for the contract is equal for each of the 6 months, you would recognize the revenues monthly. Your cash won’t align with the revenue recognized, but that’s ok. If you are providing the majority of the services at the beginning of the contract and very little in the last couple of months, you may have an argument, that you should be recognizing more revenues in the earlier months and less in the latter months. The business owner should discuss recognition of revenue with their accountant to ensure that revenues recognized in the period are matched with costs incurred to earn this revenue. This will ensure that profit margins are not skewed in any one period when costs and revenues are mismatched. Also, depending on the type of business you have, you may need to comply with a specific set of accounting standards. This should be a discussion to have with your accountant to see if this applies to you and your business.

Cost of Sales or Cost of Service

Similarly, the Cost of Sales or Service should also match the timing of the revenues. If the costs are not co-ordinated to be recognized at the same time as your revenues, you will end up with a financial story that will either present things better than they are or worse than they are. It is also important for you to recognize the true inputs that relate to generating your revenues. If you have inventory, it is also important for you to do an inventory count at the end of your period to ensure that your inventory value is correct. If it is understated or overstated, there is a good chance that your cost of sales amount needs to be adjusted.

Another input that should be reviewed are your staffing costs. Is there a portion of these costs that should be included in the cost of sales? If you have employees that help assemble your inventory, or if you have shipping costs directly related to the shipment of your goods, you should consider including these costs as a part of your cost of sales. Business owners and their accountants should discuss the costs associated with the sale of each product or service in order to get a true picture of gross profit and ensure your goods and services are priced accordingly to earn a profit. If not, what are you in business for?

Gross Profit

Gross profit is calculated by taking your Revenues less your Cost of Sales. You should always aim to have a positive Gross Profit. It is the Gross Profit that provides the funds to operate the administrative side of the business. If your Gross Profit is negative, have a look at your revenues and expenses. Have things been reflected properly? If they have, are you spending too much on your inventory? Are your prices too low? From an investment point of view, a potential investor will shy away from a company who is operating with a negative or small gross profit (or a gross loss). It demonstrates that the business owner doesn’t have a firm grasp on the market that they are selling into and are digging a hole that will eventually be too hard to climb out from.

This is why it is important to ensure that your cost of sales (or service) is calculated correctly. If the price of your product or service isn’t high enough to cover your direct inputs (costs), you will need to consider increasing your sales price.

Overhead Expenses

Overhead expenses are another word for administrative or fixed costs. These expenses relate to the administrative side of the business and would be required if you have sales or if you don’t have sales. Generally, these tend to be your fixed costs that will not vary as sales increase or decrease.

This would include things like salaries for your office staff, rent and insurance. Some costs will have a variable nature to them depending on the size of your business, such as advertising, meals & entertainment costs, travel, and interest charges. These costs are not usually directly tied to sales of your product or services and are therefore considered overhead expenses.

This does not mean that these costs should be ignored. It is a good idea to look at the trends of these costs. Are your advertising efforts matching with the increase or decrease in your business? Should you be reviewing your loans to see if you can receive a more favourable interest rate? How long is your lease agreement with your landlord? Do you expect your rent expense to increase or decrease in the coming months?

As a general rule of thumb, we also do not like to see overhead expenses exceed 10% of gross revenues. As revenues grow, we like to see this ratio decrease as we should not see any large swings in these costs in relation to revenue. If there are large variations, consider if any cost category currently classified in overhead expense should be considered in cost of sales instead. Then re-evaluate your profit margin and sales prices.

How to use or interpret your Income Statement

The income statement can be created at any point in time and should be reviewed at regular intervals. As your business is starting out, things are pretty hectic and crazy. So, potentially creating monthly financial statements is asking a bit too much for yourself in the first year or so. However, at a minimum, you should look at your income statement twice a year. Once at the halfway point during the year to check in to see how things are going and to determine whether or not you need to make any adjustments.

A budget can be created before your start your business. And a significant portion of your budget will be based on how you expect your business to perform in a year. The income statement portions of your budget can be used to compare against your current income statement. Are things turning out the way that you had hoped? Are things better? Are things not going according to your plan? Once you start looking at the numbers, start investigating what the numbers are trying to tell you.

If this is overwhelming or you’d like a bit of assistance getting started on the right path on understanding your Income Statement, reach out to your accountant to have them help you understand what is going on in your business. If the numbers just look like dollars to you and you aren’t sure what they are trying to tell you, spend the time to learn. Once you spend a bit of time understanding the information, it will make you a stronger business owner, one that can make informed decisions about your business. Don’t worry, it will get easier each time you review the financial information.

Interpreting your Financial Statements – The Income Statement Read More »

Interpreting your Financial Statements – The Balance Sheet

For a business owner, a set of Financial Statements can be an important tool in running your business. Generally speaking, there are three sets of statements that are commonly prepared by accountants. The Balance Sheet, Income Statement (Statement of Income and Retained Earnings), and the Statement of Cash Flows. In this blog post we’ll go into a bit of detail as to what information each statement can provide. By understanding these statements, you’ll have a better understanding as to the areas in your business that you are excelling at and other areas that may require more of your attention. It will also help you gain a better understanding of what other people are seeing in your business too. This is especially important when you are looking to get financing from a bank or other financial lender.

What is the Balance Sheet?

The Balance Sheet is prepared for a specific date in time. Generally, the statement is prepared at the end of a fiscal period or year-end. The purpose of the statement is to provide a snapshot of a business on a particular date. It gives an overview of a company’s Assets (Cash, Inventory, Accounts Receivable, Fixed Assets), Liabilities (Accounts Payable, Bank Loans, Shareholder Loans) and Equity (Share capital, Retained Earnings/Deficit).

Key Line Items on a Balance Sheet

Some key areas of the Balance Sheet that business owners should review regularly are Cash, Accounts Receivable, Inventory and Accounts Payable.

Cash

Cash is king/queen. It is what is going to pay for everything that you do in your business. Without it, you will need to invest more into your company or you will need to look to external parties to invest or loan you funds to give you time to make your business profitable. Monthly reconciliations of the bank balances allow you to ensure that you know how much money you have in your bank account that can be used to pay your suppliers and employees. If you have a retail business and receive payment for purchases through a credit card processor, you can use the bank reconciliations to ensure that the payments from the credit card company are being deposited on a frequent basis and that the deposits match to what you think that they should be. Reconciliations also give you and your accountant comfort that you have captured all of the transactions in the period in your accounting records. Without it, you may be able to cherry pick which transactions are recorded in your business and you may not get a true picture of your cash position.

Accounts Receivable

Accounts Receivable should be reviewed to ensure that your customers are paying you on time. If you find that you have had a record-breaking quarter in revenues, but your bank account is low, it’s likely that you have not received payment from your customers. You should be in touch with them on a

regular basis to ensure that they can still pay what they owe you. If there is an account that is not collectible, consider writing it off or at least providing a provision that it won’t be collected. If your provisions are increasing month over month, you may want to see if your pricing is appropriate or if your target markets need to shift to customers who are more likely to pay the full amount and on time.

Inventory

Inventory is another area that should also be reviewed on a frequent basis. If you have inventory, you should review to ensure that what you have in inventory, is still saleable. Is anything damaged or obsolete? Have you performed a count of all your inventory to ensure that what you think should be in available for sale is actually available? By keeping an eye on your inventory and continually checking to make sure that you have enough goods on hand and that they are saleable, will limit the possibility of theft occurring and that damaged goods or unsaleable products are identified early enough so that you can either dispose of these goods or sell them at a discount to make room for more saleable options.

Accounts Payable

Accounts Payable is the other key number on the Balance Sheet that should be reviewed regularly. This allows you to monitor what bills need to be paid in the next 30 days and what can be deferred to a later date.

Balance Sheet Financial Ratios

You will often hear in conversations amongst business owners terms like Current Ratio and Inventory Turnover. So what are these ratios and what do they tell you about a business?

Current Ratio

The current ratio determines if a business has enough funds available to pay off their operating expenses or current obligation. To calculate this amount, you would take your current assets (or items that are cash or can be quickly converted into cash, such as Cash, Accounts Receivable and Inventory) and compare this amount to the company’s current liabilities (Accounts Payable, Taxes Payable and Current portion of Debt payable) to see if the current assets are greater than the current liabilities. If the Current Assets are greater than the Current Liabilities, the lenders will gain confidence that the business can pay off their operating expenses.

Example: On December 31st, for the current assets, Cash is $5,000, Accounts Receivable is $10,000 and Inventory is $20,000. For the current liabilities, Accounts Payable is $20,000, GST Payable is $5,000, and the current portion of the debt payable is $25,000. Therefore, the current assets total to $35,000 and the current liabilities total to $50,000 and the current ratio computes to 0.70. The business owner and potential lender should start being concerned that they may not be able to pay their suppliers on a timely basis since they do not appear to have enough liquid assets available to pay their liabilities.

As a point of reference, a good target ratio is about 1.0. Most external parties will be looking for this regardless of the industry.

Inventory Turnover

The inventory turnover ratio will inform a business owner or potential lender how quickly the inventory is being sold. To calculate this ratio, you would take the Cost of Goods Sold and divide it by the Average Inventory Balance. To calculate the average inventory balance, you would take the inventory balance at the beginning the period plus the inventory balance at the end of the year and divide it by 2.

Example: On January 1st, the inventory balance is $100,000. During the year the company recognized $200,000 in Cost of Goods Sold. On December 31st, the inventory balance is $75,000. The Inventory Turnover ratio is therefore $200,000 divided by ($100,000 plus $75,000 divided by 2) = 200,000/((100,000 + 75,000)/2) which equals 2.29.

The inventory has turned over more than 2 times during the year. This business owner should be confident that the risk of having obsolete inventory is low. However, this doesn’t eliminate the need to review the inventory on hand to make sure that there isn’t any old inventory still held by the company.

Shareholder Investment

Another area that a lender will look at is how much money the business owners have invested into the business. This can be viewed by looking at the Liabilities and Equity sections of the balance sheet. If there is a large shareholder loan in the liabilities section of the balance sheet, this is an indicator of how much money the Shareholders of the company have invested into the company. If the Shareholder Loan is located in the Assets section of the balance sheet, this is an indicator that the Shareholders have withdrawn money out of the company and owe it back to the company. Lenders will often prefer to see a Shareholder Loan balance located in the Liabilities section of the balance sheet, which indicates that a Shareholder has some stake in the business and an interest in reinvesting and growing the business rather than removing all of the wealth from the company.

Interpreting your Financial Statements – The Balance Sheet Read More »

Canada Emergency Business Account (CEBA) Upcoming Repayment

Are you ready to make your CEBA Loan Repayment by December 31, 2023?

Recap of what the CEBA was for: The Canada Emergency Business Account was one of the initiatives that the Government of Canada created as a way to support business owners during the COVID-19 Pandemic. The initial support payment was a $40,000 non-interest bearing loan with $10,000 being forgivable if the amount was repaid IN FULL by its due date. There was then an additional $20,000 that became available as the COVID-19 Pandemic continued beyond what was initially anticipated. Of this additional $20,000 only $10,000 needed to be repaid. In 2021, if a business received the initial $40,000 CEBA loan, they were to include $10,000 into their income for the forgiven amount. And then if they were the recipients of the additional $20,000 loan in 2021, they were required to include $10,000 of the forgiven portion in their 2022 tax return. The initial repayment date was December 31, 2022 but then as that day approached, the government extended the payment date to December 31, 2023.

We don’t expect that there will be any more extensions on this repayment date.

If you have the funds available to repay your CEBA loan, you can pay it now or wait until closer to the December 31st deadline to make your repayments. Personally, our preference is to repay it now, so that the risk is less that you spend the funds between now and December 31st, and risk not having the money to make the required repayment.

And just to reiterate, you do need to repay either $30,000 if you received the initial $40,000; or $40,000 if you received the initial $40,000 plus the additional $20,000. If you are unable to repay these amounts by December 31, 2023, you will need to repay the full amount of the loans. Your inability to repay the $30,000 or $40,000 by December 31st, will change your repayment terms. You will need to repay the full $40,000 or the $60,000 depending on whether or not you took advantage of the second loan.

We also don’t expect any leniency on the amounts that are required to be repaid. In other words, if you owe $40,000 in CEBA repayments and you only have $38,000 available to pay by the end of December, you will be forced to actually repay $60,000 and you will actually be charged interest from January 1, 2024 to December 31, 2025. You will need to work out repayment terms with the financial institution who loaned you the funds.

If you have $37,000 available right now and need to make a repayment of $40,000. Try and budget between now and December 31st to save additionally per month to get you to the required $40,000. This savings of $500 per month will save you $20,000 in cash as well as any interest that you may have to pay.

A couple of items to note:

1) If you are unable to repay the full amount, the loan forgiveness amount that you previously included in your income for your business, can now be a deduction since the loan forgiveness no longer exists.

2) If you didn’t claim the forgiven portion as income in a previous year and you are planning to or have repaid the reduced amount in full, you do need to make an adjustment to your 2021 and 2022 tax returns for the loan forgiveness amount by increasing your income by $10,000 in 2021 if you received the $40,000 loan and $10,000 in 2022 if you received the additional $20,000. (you can’t get something for nothing).

Canada Emergency Business Account (CEBA) Upcoming Repayment Read More »

Mid Summer Planning – Looking Back and Looking Forward

June = Halfway point in the Calendar year. It’s astonishing how every year, January and February drag on a bit and then life speeds up in March and April, then May goes by relatively quickly and all of a sudden it’s June!! For the kids, it marks the end of a school year. For Public Practicing Accountants, this month is the last push to get all of the Sole Proprietor and Calendar End Corporation Tax Returns completed. But what next?

As a business owner, it may be the perfect time for you to reflect on where you’ve been. To take stock of what went well, and what can be improved upon. Use this information to plan for the next 6 months. If you were able to plan out your year, look at how close you are to what you had budgeted for. Where did you deviate from your initial plan? Do you want to get back to the original plan? Or do you like where you’re currently going?

From an accounting perspective, now is a great time to look at your financial results. And it doesn’t have to take too much out of your day to do this. Look at the information that you have and compare it to the last quarter, the last year and the last month. See if any trends are occurring. Does something look really weird? Like it’s too good to be true? Or are things inline with what you expected? If you are using an accounting software program like QuickBooks Online or Xero, you can extract this information relatively quickly. Take the time (an hour or so) to really look at the numbers. And take the time to compare these numbers to other periods (another hour). Then spend some time figuring out the story that the numbers are telling you. Is the current recession affecting you positively or negatively? Do you need to alter your purchasing schedule for your inventory? Do you need to think about extending credit to long time customers. Do you need to reduce staff? Increase staff? This part may take 2 hours or so.

Then create a plan to carry you through to the remainder of the year. And to set yourself up for planning into the following years. This part may take a bit of time, but if you spent a couple of hours working on a plan and set some concrete deadlines towards realizing these plans, you may have spent the equivalent of 6-8 hours of time on this planning process. This doesn’t have to be done all in a single day. You can do each part in isolation and stretch it out over a few days. However, I would recommend that you do accomplish this in a short amount of time (say 1 week). This allows you to keep the momentum going and to not have to revisit what you’ve already reviewed each time.

During the reflection time, be proud of what you have accomplished and appreciate the struggles that you have faced or are facing,but take an honest look at where things are not going according to your plan. And figure out what things need to be changed. Most of the time, you can work towards correcting things that have caused you to go “off track”. If you’re unsure as to what is causing you to go on an unforeseen path, chat with your management team, bring them in to help brainstorm. You have hired them in a senior position for their skills. Let them use those skills to support the business. If you are the management team, reach out to people you trust to help you explore different solutions. Ask your accountant too. Getting a different perspective can help create new opportunities.

Mid Summer Planning – Looking Back and Looking Forward Read More »

New Trust Rules and implications to Corporate Bare Trustees

On December 15, 2022, Parliament passed Bill C-32. In that bill, were some new trust reporting rules that will impact a number of people. In particular, anyone who has a Bare Trust agreement. Why is this causing a fair amount of stress for business owners and professional accountants?

Here is a bit of background:

In BC, the Property Purchase Transfer Tax is assessed each time a property is sold. Currently, the rates are 1% on the fair market value to $200,000 and then an additional 2% on the fair market value that is in excess of $200,000 to $2,000,000. And if the property is worth more than $2 million, the property purchase transfer tax increases to 3%. If the fair market value of the property is over $3 million, there is an additional 2% tax. As an example[1], if a $4,500,000 property in BC is sold, the property purchase transfer tax is $143,000.

$2,000 on the first $200,000

$36,000 on the next $1,800,000

$75,000 on the next 2,500,000 and ($4,500,000 – $2,000,000 = 2,500,000 x 3%)

$30,000 on the amount in excess of the $3M FMV ($4,500,000 – $3,000,000 = $1,500,000 x 2%)

If you are in a property development business, where properties are bought and sold as a normal course of business, this is a high cost to doing business. One way to avoid having to pay the Property Purchase Transfer Tax each time is to establish a Bare Trust agreement, where a corporation holds the legal title to the land as a Bare Trustee. The Trustee only looks after the property according to the instructions of the beneficiaries of the property. The property developers can instruct the Bare Trustee on how they want the land to be developed. If the beneficiaries (the property developer) sell the property, they will sell the shares of the Bare Trustee corporation. In this scenario, the title holder of the property doesn’t change, just the shareholders of the company. So, there hasn’t been a change in ownership of the land. So no property purchase transfer tax needs to paid to the province. Which can save a business a LOT of money. Any gain or loss on the sale of the property is taxed in the hands of the beneficiary company, so the property developer will pay the tax on the disposition of the land.

Prior to the new Trust Reporting Rules, the Bare Trustee would file an annual Corporation Income Tax Return (T2), since it is a corporation. However, with the new Trust Reporting rules, even though a corporation owns the property, the Bare Trustee agreement between the corporation and the property developing company creates a Trust relationship and are now required to file as though they are a Trust. So now the corporate Bare Trustees will need to file both a Corporation Income Tax Return and a Trust Information Return (T3).

A bare trust arrangement may also exist in many common situations where parents have added their children to title of their home for estate planning purposes or children have added a parent to title in order to qualify for a mortgage. In these instances there is no formal written agreement that sets up this arrangement as a trust arrangement, but it is in fact a bare trust, where one person holds an asset on behalf of another person, but the benefit of the asset belongs to the first person. Certain trust arrangements are exempt from this reporting requirement. Some common examples are:

- If the trust arrangement has not been in place for three months;

- If the underlying asset(s) are valued at less than $50,000 throughout the year – assets may include deposit accounts, government debt obligations or listed securities; and several more but less common to individual taxpayers.

The tricky part is figuring out if you have a trust arrangement that even needs to be considered for these reporting rules. As these situations are not well documented and most taxpayers will not even know to ask. Our firm is taking this very seriously and will be having a conversation with every one of our clients to make sure we do not miss this new form as the penalties are outrageous.

The penalties for not filing the returns are pretty high. There is the standard $25 a day, with a minimum of $100 to a maximum of $2,500. But there is also an additional penalty of the greater of $2,500 or 5% of the maximum value of the property held during the taxation year if there was a failure to file or gross negligence can be proven. So, in the case of the example above, where there is a property of $4.5M held by a Bare Trustee, if the T3 Trust Information Return is never filed, there will be the initial $2,500 penalty plus a potential additional $225,000 penalty owed for not filing for one year.

The good news is that these new rules don’t apply to 2022. They will apply for tax years ending after December 30, 2023. It is a great time to reach out to your accountants to chat about what these new reporting rules mean to you.

[1] BC government website: https://www2.gov.bc.ca/gov/content/taxes/property-taxes/property-transfer-tax/calculation-examples#:~:text=General%20property%20transfer%20tax%20rate,-See%20general%20property&text=Calculate%20the%20tax%20payable%3A,%24450%2C000%20X%202%25%20%3D%20%249%2C000

New Trust Rules and implications to Corporate Bare Trustees Read More »

What is a Dividend?

A dividend is one of the most common ways that Owner-managed businesses will distribute funds to the owners. Dividends are also distributions of their accumulated after-tax dollars that companies will give their shareholders. However, there are some key points that shareholders need to be aware of when they decide that they would like to receive dividends. Here’s a quick and dirty checklist:

- Is there a class of Shares that can pay dividends? If so, what are the rights and restrictions?

- Are there Retained Earnings available to be distributed to the shareholders?

Dividends are distributions to shareholders with after-tax corporate dollars. So if your company is in a Deficit, the company may not be able to distribute dividends. - Is there a set amount that you need to distribute as dividends for your class of shares? Or is it discretionary?

- Are you distributing Eligible or Non-eligible dividends to the shareholders?

- Do you have all of the relevant information for the shareholders? (SIN/Business Number, Address)

- Have the Directors of the company authorized the payment of the dividends, by way of a director’s resolution?

- Who is preparing the T5 Dividend Slip and Summary that needs to be filed with the Canada Revenue Agency (CRA)? If it is your accountant, please make sure that you have discussed this with them so that they are aware that these forms need to be filed.

What is a Dividend? Read More »

Bonuses – pay it out or contribute to a Group RRSP (pros & cons)

February is a month that is commonly used for paying out bonuses to employees. One of the reasons for this is so that employees can use those bonuses to contribute into their RRSPs prior to the RRSP contribution deadline. Another reason, is that it allows employees to be taxed on these bonuses in the following year, vs the previous year. Some employers will pay out this bonus directly and employees can contribute it into their own RRSP plans or employers will make the contributions into a Group RRSP that the employer establishes for their employees. There are pros and cons to both options.

| Self Administered plans Benefits | Group RRSP Benefits |

| You control where your money is invested | The company takes care of managing the plan (i.e. less work for you) |

| You can determine how much you put into a plan | Your withholding taxes from your employer are less (takes into account the deduction you’d receive for making an RRSP contribution), so more $$ is in your pocket each pay period |

| You can enlist various advisors to assist with making decisions about where your money is invested | As the withholding taxes are reduced with the contribution, you can put more money into your RRSP right away rather than waiting for next year’s tax refund |

| Self Administered plans Cautions | Group RRSP Cautions |

| It can be more time consuming for you | You don’t control how your money is invested |

| You may forget to deposit an amount into your plan | There could be some restrictions on what happens when you leave your company. |

| What your money is invested in may be restricted to certain types of investments |

Bonuses – pay it out or contribute to a Group RRSP (pros & cons) Read More »

Fresh Starts: Assembling your Year-end info. What does my accountant need to file my Business Taxes?

Happy New Year! January is a time for Fresh Starts. For your business, it’s also a time to reflect on how the year went. And as Accountants, its now the beginning of the time when we start reaching out to our clients to remind them of what we’ll be needing in order to prepare their corporate tax returns.

Here’s a snapshot of the checklist that we’ll generally send out to our new clients. What I’m adding though is some of the reasoning behind the requests.

1) Two years of historical tax returns, financial statements, and notices of assessments – both corporate and personal

a. This allows us to get a general idea of how your business is doing and to gain a better understanding of how your business operates.

b. This also allows us to see where there are potential tax and accounting treatments that could be more advantageous for you and your company.

2) Any legal agreements outstanding for the company

a. For accounting and tax purposes, this allows us to understand if there are any liabilities that need to be recorded, and any potential liabilities that may be arising in the future.

i. This supports us in our helping you plan your cash flow and also for some potential tax planning.

3) Minute book, including certificate of incorporation as well as supporting schedules, share register, bylaws, shareholder agreement (if applicable)

a. For many small businesses, there is a tendency for business owners to self-incorporate. While this is a legitimate way to incorporate, there is a tendency to forget or be unaware that there are certain documents/agreements that need to be in place in order to ensure that the business is properly incorporated.

i. The most common mistake is that shares are not issued. Shares are the asset that each shareholder should hold. This piece of paper is what is needed to indicate that the company is owned by someone.

b. The minute book is a record of the actions that the directors of the company have approved.

i. Common documents in the minute book are:

1. The appointment of directors

2. Resolutions approving any issuance of dividends

a. The type of dividend that have been approved.

4) A copy of the bookkeeping file and password (i.e. Quickbooks Desktop/Sage) or an invitation sent to [email protected] to access the accounting system if it is web-based (i.e. Quickbooks Online, Xero, Wave).

a. This is to allow us to generate reports like the Balance Sheet, Profit & Loss Statement, and Trial Balance

i. These are reports that we will use to create your financial statements and tax return.

b. It also allows us to focus on the entries that make up a balance in the accounting records without having to ask you about it, which allows us to be as efficient as possible

5) Year-end bank reconciliation and bank statement for all bank accounts

a. This allows us to see that you have performed a reconciliation of your cash accounts and that you understand what cheques have not been cashed, or what funds have not been received.

6) Inventory count documentation at year end (if applicable)

a. This allows us to ensure that what you have on your books matches what you actually have in inventory

7) Investment portfolio statement for marketable securities held by the corporation;

a. For accounting and tax purposes, we need to know if there are any realized or unrealized gains or losses in your portfolio.

b. We will also need the Foreign Reporting statement that your Financial Institution provides you with as there is a separate Tax Form (T1135) that may need to be completed and submitted to the CRA>

8) Copies of insurance policies if insurance has been prepaid for the year;

a. This allows us to determine if a portion of the insurance that was paid in the year, should still be recorded on your books. If there is a portion of the policy that hasn’t expired by the end of your fiscal year-end, this amount would need to remain on your books as a prepaid expense.

i. Example. You pay your insurance on an annual basis. But the insurance period is from October to September each year. You have a calendar year-end. Therefore, in December, you should have on your Balance Sheeet 9 months worth of a prepaid expense (Jan – Sept) since this portion of your insurance policy hasn’t been used.

9) Purchase agreements and/or bills of sale for any capital assets acquired or disposed of during the year.

a. Certain capital assets, like vehicles, have restrictions on how much can be capitalized for tax purposes. Therefore, having the purchase agreements allows us to determine how much can be capitalized on your tax return.

b. This also allows us to determine if any leased assets should be treated as a capital or operating lease for accounting and tax purposes.

10) Year-end credit card reconciliations and credit card statements